Treasuries get a ton of attention due to their liquidity and perceived safety, but for those willing to take on some credit risk, you can attain decent yields with investment-grade corporate debt.

However, for both advisors and retail investors, gaining exposure isn’t as straightforward as logging into TreasuryDirect or buying T-bills at a broker. While numerous ETFs are available, they all have some shortcomings when it comes to meeting the needs of advanced investors. Here are some roadblocks you may run into, and how a new, innovative lineup of corporate bond ETFs from F/m Investments seeks to solve them.

Buying individual corporate bonds

Imagine you’re an advisor or a retail investor who primarily deals with stocks. You’ve grown accustomed to the straightforward process of buying and selling shares on an online platform with a few clicks. Now, consider the experience of buying an individual corporate bond.

First, there’s the issue of the over the counter (OTC) market. Unlike stocks traded on centralized exchanges with transparent pricing, corporate bonds are traded OTC. This means you have to navigate through brokers and dealers to find the best price.

There’s no single, centralized place to view real-time prices, making it challenging to ensure you’re getting a fair deal. This lack of centralized pricing adds a layer of complexity to your investment strategy.

Next, think about liquidity. Stocks can be bought and sold with ease, but corporate bonds are not as liquid. The OTC market means that finding a buyer or seller can take time, and prices may fluctuate more between trades due to the lack of continuous trading. This illiquidity can be a significant hurdle if you need to quickly sell a bond.

Additionally, corporate bonds typically pay interest semi-annually. This can be a drawback compared to stocks, which may offer quarterly dividends or other more frequent income. For those relying on regular income streams, the semi-annual payments from bonds can be less convenient.

Each of these factors—over-the-counter trading, lack of centralized pricing, and semi-annual interest payments—can be pain points when it comes to liquidity, accessibility, and income consistency.

Investing in corporate bond ETFs

Corporate bond ETFs address some of the challenges of individual bond investing. They swap semi-annual interest payments for more frequent monthly distributions and allow for trading like stocks with bid/ask spreads, providing more liquidity and ease of access. However, these ETFs also introduce new challenges.

First is the problem of “diworsification.” Sometimes, more is not better. When a corporate bond ETF samples from, say, 2,774 issues to replicate its index, you’re no longer getting targeted exposure to the specific issuers or industries you want.

Instead, you often end up with an overweight position in sectors like banking which is notorious for being a “serial issuer” of bonds that ends up dominating many indexes, which might not align with your investment goals or risk tolerance.

Second, you’re no longer targeting a specific maturity. These ETFs constantly turn over their holdings to replicate an index benchmark in aggregate. This means the bonds within the ETF are regularly bought and sold to maintain the desired index characteristics, instead of capturing the latest issues only.

As a result, you don’t get the precise maturity exposure you might want. For instance, if you’re looking to hold bonds with three years maturity, the constant turnover and sampling strategy in a bond ETF can make this strategy difficult to implement.

These issues highlight why, despite solving some problems, corporate bond ETFs may not fully meet the needs of all investors.

The solution

F/m’s lineup of equally-weighted corporate investment-grade ETFs seeks to solve most of these issues by retaining the best of both worlds. The three ETFs in this lineup are:

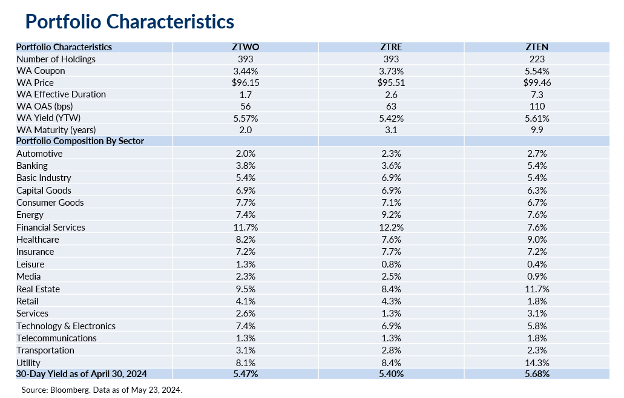

- F/m 2-Year Investment Grade Corporate Bond ETF (ZTWO)

- F/m 3-Year Investment Grade Corporate Bond ETF (ZTRE)

- F/m 10-Year Investment Grade Corporate Bond ETF (ZTEN)

Here’s how they work: each ETF rebalances monthly to maintain its target maturity term and participates in the new issue market to capture the current market coupon.

In other words, when you buy ZTWO, for instance, you’re getting targeted exposure to the 2-year portion of the yield curve, and not just a portfolio of 1,000 bonds averaging out to that maturity. Each ETF diversifies by targeting an equal-weighted portfolio of investment-grade corporate issues, with each bond making up around 0.25% of the portfolio. This results in a far lower allocation to the financial sector and more even representation across other industries.

You still get the usual monthly distributions of bond ETFs and the liquidity benefits. For example, ZTWO has a 30-day median bid-ask spread of just 0.04%, making it easy to size and enter/exit positions. All of this comes with a 0.15% expense ratio, competitive with existing bond ETFs like the iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD), which charges 0.14%.

Trade ideas with these ETFs

Here’s something you can do with these ETFs that would be difficult with individual bonds: selling them short. A trade idea you could implement by selling an equally-weighted corporate investment-grade ETFs short while going long on a single-bond Treasury ETF of the same maturity is called a “credit spread trade.”

How It Works

- Identify Maturities:

- Execute the Trade:

- Go Long on the Treasury ETF: Buy shares of the Treasury ETF to gain long exposure to U.S. government debt.

- Short the Corporate Bond ETF: Sell shares of the corporate bond ETF to gain a short position in corporate debt.

The Goal

The primary goal of this trade is to profit from the widening or narrowing of the credit spread, which is the difference in yield between the corporate bonds and the Treasury bonds of the same maturity.

- Expecting Credit Spread Widening:

- If you anticipate economic conditions will worsen, corporate bond yields might rise relative to Treasury yields due to increased credit risk. In this case, the value of the corporate bond ETF might fall relative to the Treasury ETF.

- You would profit from the short position in the corporate bond ETF as its price declines and from the relatively stable or rising price of the Treasury ETF.

- Expecting Credit Spread Narrowing:

- Conversely, if you believe the economic outlook will improve and credit risk will decrease, corporate bond yields might fall relative to Treasury yields. In this case, the value of the corporate bond ETF might rise relative to the Treasury ETF.

- In this case, you would simply inverse the previous trade idea by shorting UTEN and using the proceeds of that short sale to take a long position in ZTEN.

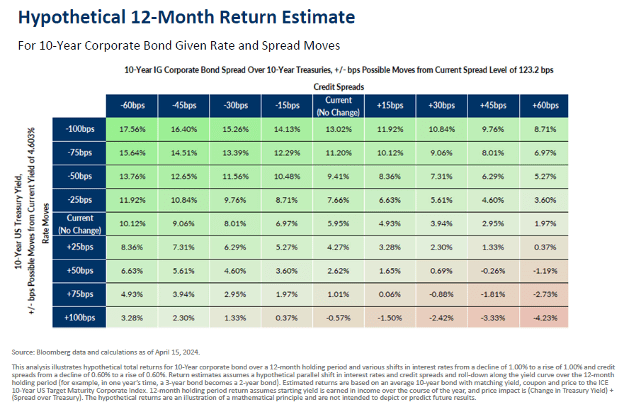

This strategy allows you to bet on the relative performance of corporate bonds versus treasuries without taking a directional bet on interest rates as a whole, all via the convenience of an ETF. Here’s a handy chart that illustrates this dynamic:

Please note this article is for information purposes only and does not in any way constitute investment advice. It is essential that you seek advice from a registered financial professional prior to making any investment decision.

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. For a prospectus or summary prospectus with this and other information about the Fund, please call (888)123-4589 or visit our website at www.fminvest.com. Read the prospectus or summary prospectus carefully before investing. Investing involves risk; Principal loss is possible.

Fixed-Income Market Risk. The market value of a fixed income security may decline due to general market conditions that are not specifically related to a particular issuer, such as real or perceived adverse economic conditions, changes in the outlook for corporate earnings, changes in interest or currency rates or adverse investor sentiment generally. Interest Rate Risk. Interest rate risk is the risk of losses attributable to changes in interest rates. In general, if prevailing interest rates rise, the values of debt instruments tend to fall, and if interest rates fall, the values of debt instruments tend to rise.

Income Risk. The Fund’s income may decline if interest rates fall. This decline in income can occur because the Fund may subsequently invest in lower yielding bonds as bonds in its portfolio mature, are near maturity or are called, bonds in the Underlying Index are substituted, or the Fund otherwise needs to purchase additional bonds.

New Fund Risk. The Fund’s is a newly organized, management investment company with no operating history. In addition, there can be no assurance that the Fund’s will grow to, or maintain, an economically viable size, in which case the Board of Directors (the “Board”) of The RBB Fund, Inc. (the “Company”) may determine to liquidate the Fund.

High Portfolio Turnover Risk. In seeking to track the Underlying Index, the Fund may incur relatively high portfolio turnover. The active and frequent trading of the Fund’s portfolio securities may result in increased transaction costs to the Fund, including brokerage commissions, dealer mark-ups and other transaction costs, which could reduce the Fund’s return.

Liquidity Risk. Certain securities held may be difficult (or impossible) to sell at the time and at the price the Adviser would like. New Fund Risk. The funds are newly organized, management investment company with no operating history.

Coupon. Is the interest payment received by a bondholder from the date of issuance until the date of maturity of a bond.

Bid-ask spread. Difference between the prices quoted (either by a single market maker or in a limit order book) for an immediate sale (ask) and an immediate purchase (bid) for stocks, futures contracts, options, or currency pairs in some auction scenario.

References to other securities is no an offer to buy or sell.

Fund may be susceptible to an increased risk of loss, including losses due to adverse events that affect the Fund’s investments more than the market as a whole, to the extent that the Fund’s investments are concentrated in a particular issue, issuer or issuers, country, market segment, or asset class. While U.S. Treasury obligations are backed by the “full faith and credit” of the U.S. Government, such securities are nonetheless subject to credit risk (i.e., the risk that the U.S. Government may be, or be perceived to be, unable or unwilling to honor its financial obligations, such as making payments).

F/m Investments is an investment advisor registered under the Investment Advisers Act of 1940. Registration as an investment advisor does not imply any level of skill or training. The oral and written communications of an advisor provides you with information about which you determine to hire or retain an advisor. For more information, please visit advisorinfo.sec.gov and search for our firm name. This presentation has been provided for informational purposes only and is not intended as legal or investment advice or recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable, though its accuracy is not guaranteed. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of publication and are subject to change without notice. Past performance is not indicative of future results.

US Credit Series ETFs are distributed by Quasar Distributors, LLC.